ARCHIVED CONTENT

You are viewing ARCHIVED CONTENT released online between 1 April 2010 and 24 August 2018 or content that has been selectively archived and is no longer active. Content in this archive is NOT UPDATED, and links may not function.Extract from article by Richard Caplan

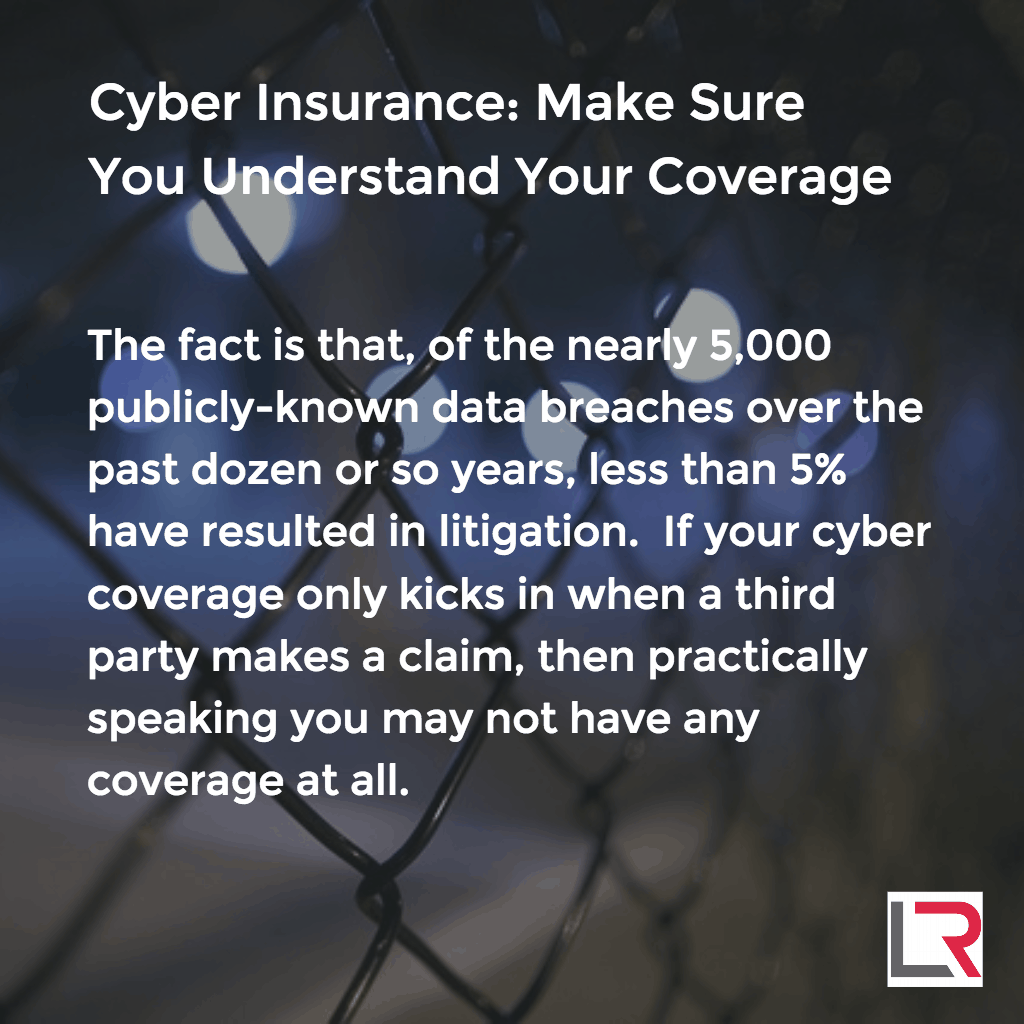

Today, businesses are increasingly purchasing cyber-specific insurance in an effort to mitigate the financial impact of a breach or other cybercrime. In terms of what might be covered in a cyber insurance policy, there are basically two types of coverage – “first party” coverage and “third-party” coverage. First party coverage covers the types of losses that your company might suffer directly in the event of a data incident. That may include losses, some of which may be covered and some not, such as data destruction, denial of service attacks, incident response, crisis management, public relations, forensic investigation, remediation, breach notifications, credit monitoring, data restoration, business interruption, lost intellectual property, theft and extortion, or damage to reputation. Third party coverage refers to coverage for claims that may be made by third parties against your company arising out of a data incident, such as data breach lawsuits, for example.

Read the complete article at Cyber Insurance: Make Sure You Understand Your Coverage