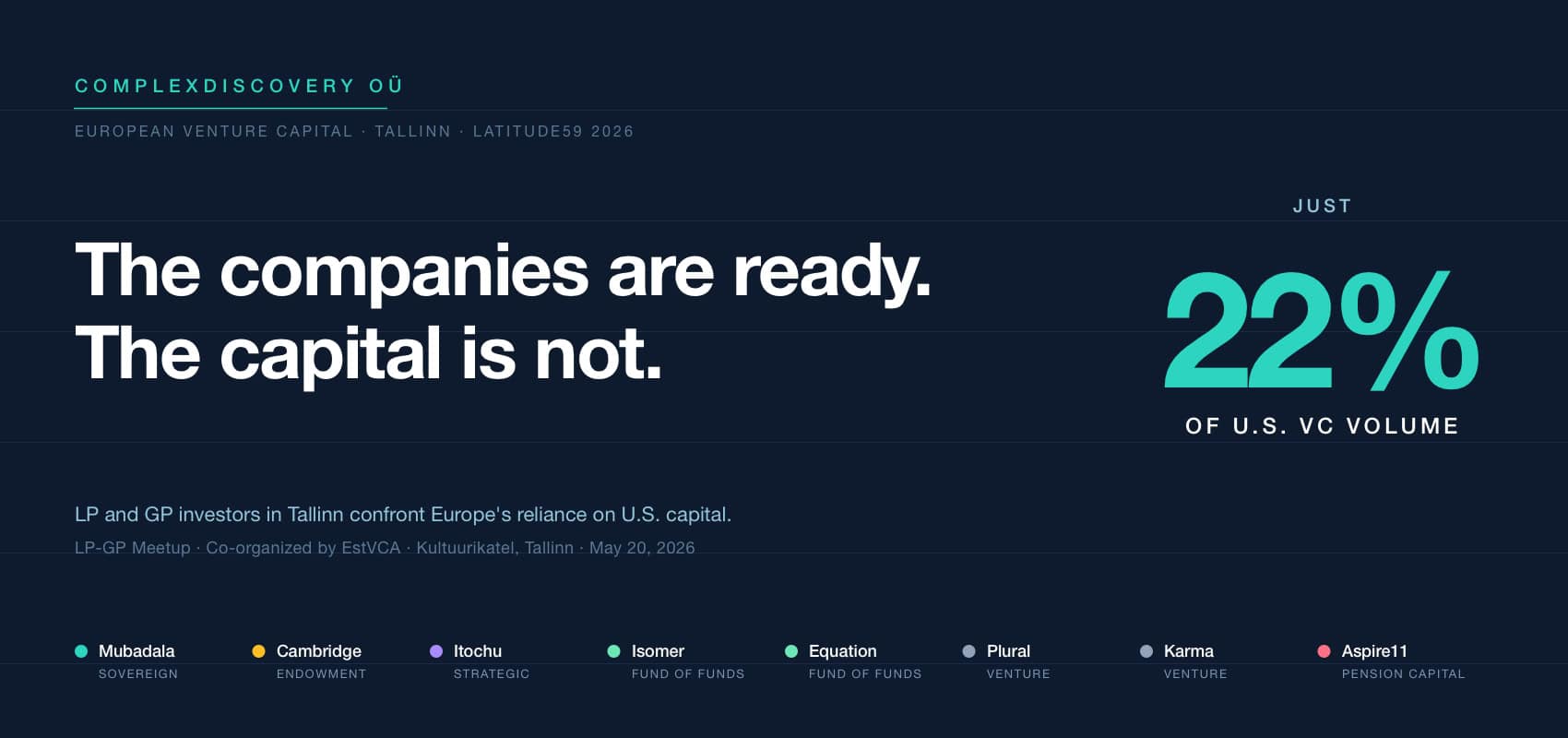

Editor’s Note: European venture investors delivered a blunt self-assessment in Tallinn: the continent can build globally competitive technology companies but still struggles to fund them at scale without American capital. During the LP-GP Meetup at Latitude59, fund managers and allocators ranging from Mubadala to the Cambridge University Endowment Fund described a deep pipeline of scale-ready companies alongside a venture market that operates at a fraction of U.S. volume.

For cybersecurity, data privacy, regulatory compliance and eDiscovery professionals, the implications are practical. Investor geography influences where vendors incorporate, where data resides and how long companies remain independent, all factors that can affect vendor risk assessments, procurement decisions and data-sovereignty commitments. The panelists’ view that deep tech and defense are becoming Europe’s strongest investment themes also offers an early signal of where the next generation of security and resilience technologies may emerge.

Watch two developments: whether pension-backed vehicles such as Aspire11’s €500 million fund can unlock institutional venture capital at scale across Europe, and whether governments respond to calls from leaders such as Wise co-founder Taavet Hinrikus for stronger support of European innovation. Both questions will determine whether Europe can match its technology ambitions with the capital to sustain them.

Content Assessment: European investors see a strong pipeline and a capital gap at home

Information - 93%

Insight - 92%

Relevance - 90%

Objectivity - 90%

Authority - 92%

91%

Excellent

A short percentage-based assessment of the qualitative benefit expressed as a percentage of positive reception of the recent article from ComplexDiscovery OÜ titled, "European investors see a strong pipeline and a capital gap at home."

Industry News – Technology Beat

European investors see a strong pipeline and a capital gap at home

ComplexDiscovery Staff

Europe has the companies. What it still lacks, investors gathered in Tallinn said, is homegrown capital willing to fund them at scale.

That assessment came from the limited partners and fund managers who met at the LP-GP Meetup, an invitation-only gathering held May 20 during the Latitude59 technology conference in the Estonian capital, according to an organizer-issued summary of the discussions released Tuesday. The group described a deep bench of European companies capable of competing globally, matched against a funding base that still leans on the United States.

The meetup, organized by the Estonian Private Equity and Venture Capital Association (EstVCA) with support from Startup Estonia and the state-backed fund investor SmartCap, drew institutional investors, fund-of-funds managers and venture firms including Mubadala, the Cambridge University Endowment Fund, Itochu Corporation, Isomer Capital, Equation, Plural, Aspire11, Karma Ventures and Siena Secondary Fund.

“Our aim was to create a high-quality, targeted platform for meaningful discussions,” said Madis Lehtmets, managing director of EstVCA. Public funding works well in Europe today, he said, but the growth of funds operating in the Nordic-Baltic region depends on attracting private capital, and the industry needs to think about how to raise European investors’ willingness to commit to funds based there.

Deep tech leads a strong pipeline

The session opened with a conversation between Taavet Hinrikus, the Wise co-founder who later co-founded the venture firm Plural, and Margus Uudam, founding partner of Karma Ventures. Both said Europe holds a strong pipeline of companies positioned to scale, with the greatest growth potential concentrated in technically demanding fields: deep tech, hardware, robotics and defense.

Estonia’s own trajectory served as the proof point. “When we were building Wise, nobody wanted to invest in regulated industries because they were considered too complicated. Now nobody is afraid of that anymore,” Hinrikus said.

Finding non-US money takes years, not meetings

Funding those companies from inside Europe is another matter. “We are making an extra effort to find more non-US investors, but it is difficult to find European investors, and they take much longer to convince,” Hinrikus said. “I also spent some time in Japan, but it feels like you have to go there three years in a row just to build relationships before anyone will take you seriously.”

The numbers behind that frustration are stark. Venture investment across Europe reached €66.2 billion in 2025, about 22 percent of the U.S. total, Josh Lerner, a Harvard Business School professor, wrote in a Feb. 20, 2026, column for the Centre for Economic Policy Research’s VoxEU, a gap he found striking given that the two economic blocs are comparable in scale. Atomico’s State of European Tech report, published in November 2025, found that almost half of the funding for European late-stage startups came from U.S. and Asian investors, a figure the venture firm repeated in a January 2026 call for pension reform.

Hinrikus traced part of the gap to attitudes toward risk. “If you fail in Europe, everyone writes you off and nobody wants to work with you again, which is the opposite of the US,” he said. The same logic applies inside institutions, he argued, where a decision-maker’s upside for backing a winning fund is limited while the consequences of a wrong choice can be severe. “I do think we need more government help to allocate more capital to the European innovation sector, because the continent needs us,” he said.

What allocators say they need

A panel on fund-of-funds strategy brought together Chris Wade, co-founder of Isomer Capital, a London-based fund of funds; Mark Schmitz, founder of the Germany-based fund of funds Equation; and Pavel Mucha, founder of Aspire11, a Prague-based firm that launched a €500 million pension-backed global fund in September 2025.

Schmitz said Equation sees the strongest potential in deep tech, naming biotechnology and space among the fields it watches. The firm revisits its sector priorities every five years, he said, weighing where strong exits could emerge a decade later. “When we see a manager in Europe who meets the very high bar and rare potential we would expect from the US, the most competitive market in the world, we will definitely come on board. If we cannot find that, then we will allocate some money in the US,” he said. Schmitz added that Equation is not prepared to invest in China at present, even though he ranks its innovation output among the world’s leaders.

Mucha said money is moving into early-stage venture funds as well as the next generation of high-growth companies, but pension capital arrives with conditions attached. “If we want to bring pension capital into venture capital, we need to balance risk, reward, and liquidity for them,” he said.

For fund managers courting institutional capital, the practical takeaways were consistent across the panel: disclose liquidity terms early, benchmark performance against U.S. peers rather than regional ones, and budget for diligence cycles that run longer with European institutions than with American funds.

A bullish long view from Isomer

Wade closed the discussion with a forecast. “European venture capital is going to become one of the most important venture capital ecosystems in the world. I have no doubt about that,” he said. In his view, Europe will produce a trillion-dollar company within the next five years, a forecast that sits at the bullish end of investor sentiment rather than reflecting any consensus market projection.

Wade recalled that when Isomer started, Europe had about 20 companies valued at $1 billion or above, and a forecast at the time that the number would reach 400 within a decade has nearly held. Industry counts support the recollection: trackers now put Europe’s unicorn total above 400, though tallies vary by methodology. The U.S. advantage, Wade said, comes down to a head start. He argued the American venture system has simply been operating twice as long, and that Europe today is ahead of where the United States stood at the same point in its own development.

Why capital geography matters for legal and security buyers

The funding patterns described in Tallinn shape the vendor market that cybersecurity, information governance and eDiscovery professionals depend on. When a European security or legal technology company raises growth rounds from U.S. funds, decisions about headquarters, governance, eventual exit and, in some cases, data residency can be influenced by investor geography, particularly where investors hold board seats or push for U.S.-aligned corporate structures. That dynamic carries direct consequences for buyers weighing data-sovereignty commitments in vendor contracts, though plenty of European vendors maintain strict European data boundaries regardless of who sits on the cap table. Procurement and vendor-risk teams should treat investor geography as a due-diligence data point alongside financials and certifications.

Two developments deserve watching. Defense and deep tech now sit at the top of European investors’ priority lists, which signals where the next wave of security-adjacent tooling will emerge. And if pension-backed vehicles such as Aspire11’s fund succeed in pulling European institutional money into venture, the ownership profile, and the stability, of the region’s technology vendors could shift within a fund cycle.

Europe’s investors say the companies are ready and the capital is not. For professionals whose vendor stack increasingly comes from European deep tech, the question is direct: does it matter to your risk model where your vendors’ money comes from?

News sources

- Latitude LP-GP Meetup | Tallinn, May 20, 2026 (Latitude59)

- The venture capital challenge for Europe (CEPR VoxEU)

- Europe creates global value. Now regulators need to help us keep the rewards (Atomico)

- 10 key findings from Atomico’s State of European Tech report (Sifted)

- Aspire11 launches €500M pension-backed fund (Tech.eu)

- Equation is a fund of funds that wants to back Europe’s emerging VCs (Sifted)

- Madis Lehtmets appointed Managing Director of EstVCA (EstVCA)

- Wise founder and Plural partner Taavet Hinrikus on scaling European deeptech (Sifted)

- Inside Isomer: Chris Wade on AI’s potential, the power of small funds, and the future of VC (Vestbee)

Assisted by GAI and LLM Technologies

Additional reading

- Nine months across Europe’s tech-sovereignty arc, from Tallinn to London (ComplexDiscovery)

- The flame and the frontier: how Estonia carries a 1919 victory into a tense 2026 (ComplexDiscovery)

- Estonia aims to be first to give AI agents official digital IDs (ComplexDiscovery)

- Britain bets billions on sovereign AI as London Tech Week opens (ComplexDiscovery)

- Ireland’s AI regulator role gets a hard look at Dublin Tech Summit (ComplexDiscovery)

- When you can’t trust the evidence: deepfakes force a forensic reckoning in Dublin (ComplexDiscovery)

- Latitude59 final day in Tallinn: AI sovereignty, a driverless permit and €450,000 to three startups (ComplexDiscovery)

- Estonia opens Latitude59 with sandbox framework for legal exemptions (ComplexDiscovery)

- FutureLaw 2026 closes: hard truths, the billable hour, and what gets built next (ComplexDiscovery)

- FutureLaw 2026 opens in Tallinn with a sharp question: who governs the governors? (ComplexDiscovery)

- The Sovereignty Paradox: Europe’s $4 Trillion Tech Dilemma at Slush 2025 (ComplexDiscovery)

- How Finland Is Reshaping Defense: BORDERLAND at Slush 2025 (ComplexDiscovery)

- Kaja Kallas Warns of Democracy’s Algorithmic Drift at Tallinn Digital Summit (ComplexDiscovery)

- Defending the Digital Frontier: European Nations Forge Resilience Against Relentless Cyber Warfare (ComplexDiscovery)

- Tallinn Digital Summit 2025 to Focus on Secure AI Futures, Cyber Resilience, and Digital Transformation (ComplexDiscovery)

Source: ComplexDiscovery OÜ

ComplexDiscovery’s mission is to enable clarity for complex decisions by providing independent, data‑driven reporting, research, and commentary that make digital risk, legal technology, and regulatory change more legible for practitioners, policymakers, and business leaders.